Where do I invest my own money?

Y'all keep asking what I do with my own money, so here's the answer (you NOSY PARKERS).

Just kidding! I totally get the inquisitiveness. Snooping on what other people do with their money is one of my favourite activities, too. It's like taking a peek inside somebody else's underwear drawer.

Where I put my money might not be right for you! Personal finance is personal by definition, and you've got to build a plan for yourself based around your own goals and needs. Here's a more comprehensive list of savings accounts and investment funds that will help you find the right one for you. The "get the right accounts" chapter in my money book is a thorough guide to identifying the right products for your own damn self.

Some stuff about my financial life that's weird:

- I have assets & expenses in both South Africa and the UK, and most of my income comes from the United States, so forex conversion is my life.

- I hate admin and err on keeping my portfolio as simple as possible (I mostly fail at this goal, as you'll see below).

- I'm fairly nomadic so I don't own a house, nor intend to buy one for the next decade at least. I'm currently living in the UK but might not be a couple of years from now, who knows!

- I'm 33, don't have/want kids, and have a long-term unmarried partner. We have one joint account for household bills but otherwise maintain separate finances.

- I work for myself.

- I prefer to maintain a slush fund rather than save up for individual savings goals.

- I have been exceptionally lucky in my life. I promise you, I count my blessings every day.

- I'm a chronic over-sharer (obvs).

This is not advice, and your mileage may vary.

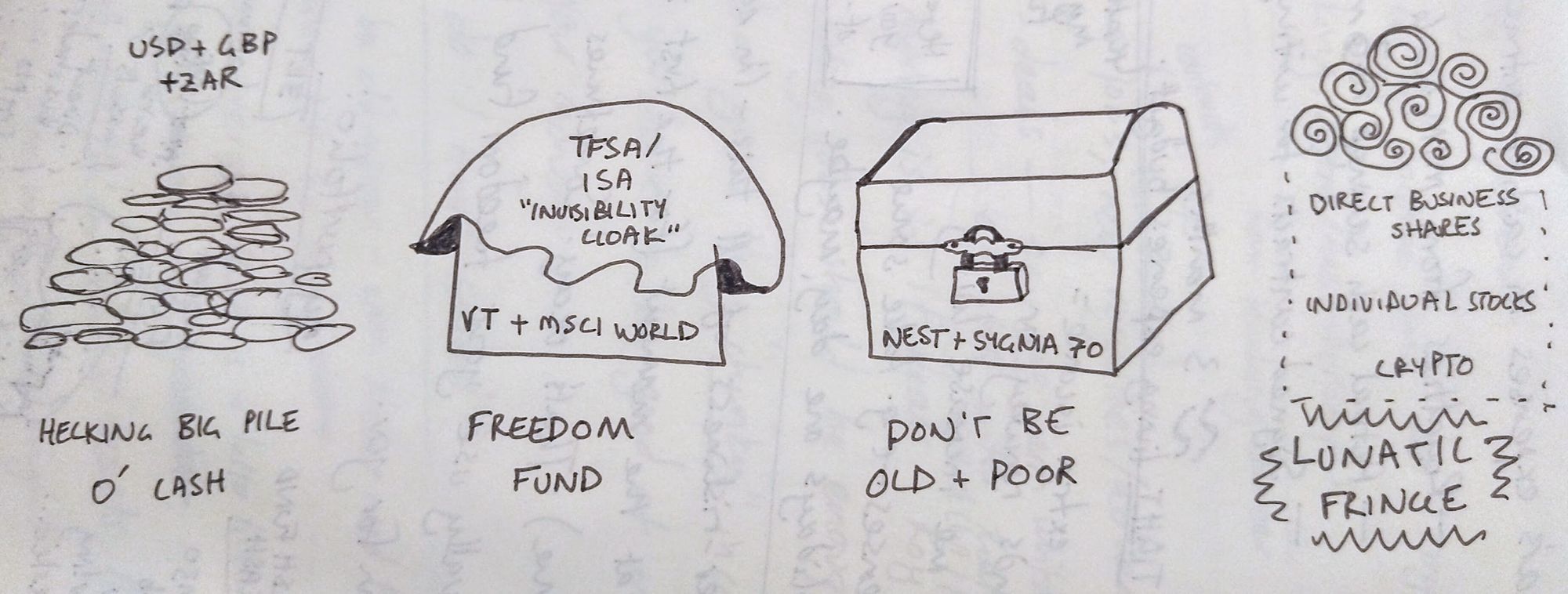

My financial life looks like this at the moment (not to scale):

Hecking big pile o' cash

I have a career with lumpy income (many months nothing, some months a lot) so I have a bigger pile of cash than most people need. At the moment, I'm trying to maintain my cash pile at about 6 months worth of expenses. I also have another 6 months worth of committed work (i.e. signed contracts) so it's about 12 months worth of secure runway.

This money is for spending, so it hasn't felt worth over-optimising the interest rates I get on it (and interest rates in the UK are basically nothing). Right now, this cash is just sitting in bank-linked savings accounts earning minimal interest. I will probably spend some time hunting down better interest rates for this cash soon, but setting up UK business accounts and breaking my SA tax residency has used up my tolerance for admin recently!

Business cash management

I registered a limited business in the UK for my writing/freelancing income, that has its own bank account. I pay myself a salary out of that business of £732 a month, and any other money I take out as dividends, because that optimises my taxes and NI contributions. Here's a video explaining why.

My business has a Transferwise account that I use to receive money from the U.S. and convert it into GBP. It's also useful for paying contractors in other countries. I use Stripe for card processing.

Xero is my business's accounting tool, and I need the multicurrency feature so I'm on a pretty expensive tier (blah). Freshbooks is apparently a better designed app, but I've been using Xero for years and just didn't feel like learning a new accounting tool.

I have a business bank account with Starling. I initially opened a Monzo Business account but it was missing some essentials for me (like the ability to receive international payments).

Personal cash management

I use Monzo for day-to-day banking and my joint account with my partner. I pay for Monzo Plus and get 1% AER on any cash sitting in that account. Monzo is magic! If you'll need a business account at some point, though, I'd recommend using Starling for both your personal and business accounts (that's what I wish I'd done, but now I'm too lazy to switch).

I've kept one South African bank account open. I use Shyft when I need to move money from SA to the UK.

I have been looking for a replacement 22seven money aggregation tool that supports accounts from all around the world, but everything I've tried so far SUCKS. I've had to revert back to using Google Sheets like a FOOL (and built in a whole multicurrency conversion layer into my money dashboard). It's bloody awful.

Freedom Fund

You've heard me wax poetical about the beauty of global ETFs. That's where I invest my Freedom Fund (long-term investments with no specific objective, just designed to let me make outrageous decisions like try to be a full-time fiction writer instead of having a real job).

I keep this simple. I have an SA freedom fund and a UK freedom fund. Moving investments costs money, so I intend to just keep my old SA funds where they are.

- UK: the Vanguard FTSE Global All Cap Index Fund (accumulation) that I buy through Vanguard directly.

- SA: the Satrix MSCI World ESG ETF that I buy through EasyEquities (it used to be the plain Satrix MSCI World ETF before they launched the ESG version).

I use my TFSA/ISA tax-free allowances for these Freedom Funds. The TFSA/ISA allowance is like an invisibility cloak that hides your investments from the taxman (legally), but you have annual/lifetime limits about how much you can put under the invisibility cloak. Please use your TFSA/ISA limits for long-term investments rather than short-term savings.

Don't Be Old & Poor

You get a tax discount for using special retirement funds for money you won't touch until you're old, but these accounts are also less flexible. I only invest a portion of my long-term investments in them. My tax guy helps me work out how much to put in every year (get a tax guy if your financial life is complicated; tax rules make zero sense).

- SA: I invest in the Sygnia Skeleton 70. It's got low fees and close to the max offshore/equities allowances. Stealthy Wealth has a great writeup about this.

- UK: I've got a small pension pot invested through Nest, initially set up through my ex-employer. I chose their Ethical Growth fund. I might move this to a Vanguard SIPP later this year.

The Lunatic Fringe

A confession: I do own some random assets from the lunatic fringe of investing. My approach to these assets is to basically pretend that I don't own them. I don't take them into account when I plan my finances, and I try to limit them to around 5% of my overall portfolio. I regard these assets as lotto tickets that might one day pay off, but are mostly just there for my entertainment.

Crypto

I worked in fintech, which means I'm one of those assholes who owned like 3 Bitcoin back in 2015 and spent them on beer and pizza.

I have continuously sold down my crypto holdings over the years to rebalance them back down to about 5% of my portfolio (moving the cash into my much safer World ETFs instead). Yes, this means I've theoretically lost an enormous amount of hypothetical money over the years, but it also means that I've maintained a risk level that allows me to sleep at night. It's not a bad strategy overall.

Also, let me tell you, even as somebody who's worked in this space and understands it quite well, I've bought my fair share of shitcoins over the years that are now worth zero. Hence the wisdom of never counting on your speculative assets, and never investing more than you can bear to lose.

Currently, I own small amounts of BTC, BCH, ETC, ETH, XRP, IOTA and XTZ.

Please don't ask me to talk about crypto. I have complicated feelings about crypto.

Individual shares (stonks)

Sometimes I buy a tiny amount of an individual stock, mostly just to remind myself how bad I am at picking stocks. My current holdings are:

- Famous Brands (because of my devotion to Steers) doing awfully, thanks Covid

- Netflix, doing fine, thanks Covid

- Canopy Growth (getting in on that sweet sweet marijuana money), doing poorly because I bought in at the height of the hype bubble like an idiot - hear me, r/WallStreetBets?

- Nvidia (mostly because of self-driving cars), doing great

I do not recommend buying individual shares. Everybody thinks they are better at this than they are. The data says that even professional share pickers are not good at this. If you're going to be a fool like me and buy shares anyway, limit it to tiny amounts you can afford to lose.

Direct business shares

Lastly, I own shares in some small tech businesses that I cofounded with my buddies. Valuing businesses is dark magic so I basically never do it. I don't include their value on my own money dashboard, because they are too high-risk to count on. Hope for the best, plan for the worst, I say!

I think the same way about things that I write. Over a writer's career, what you're trying to do is build up a portfolio of assets (books, short stories, comics, whatever) that will hopefully pay dividends for you, for as long as possible. Being an artist means being an entrepreneur, just one with even wilder odds of success. I'm pessimistic by nature, so I don't include these assets on my money dashboard either. I try to make sure that I'm not going to be old and poor (my #1 financial goal always) even if I never earn a single cent from any of these assets.

If you have the appetite for it, starting your own business is probably the single most impactful way to build wealth over a few years. But it's also really not for everybody.

There you have it, you inquisitive busybodies! I hope you enjoyed this look inside my financial underwear drawer. Feel free to ask any clarifying questions, and remember that what works for me will be different to what works for you.

Mega smooches

Sam

Member discussion