Should you split up your savings?

Today we're taking a question from one of our readers who wants advice about whether to split up his savings.

So I read your book last year and have been following the step by step guides. I have gotten rid of all my debt, got a small emergency fund going and got an RA and TFSA. My question is with regards to short term savings accounts.

When saving for the short term, do you put all of the money in one account or multiple accounts? For example, say I want to save for council fees, car maintenance, new Nike running shoes, and a new iPad. If I put them all in one account, my monkey brain sees a big number and is like, cool what can I buy, or I have no idea how much I saved for the new Nikes.

Also, holiday savings. So I'd like to go on multiple local trips a year as well as an overseas trip every few years. Would you separate each holiday (local holidays) into different accounts or just one big one?

Dear reader, your seemingly simple question is actually scratching at one of the deepest and most perplexing questions in behavioural economics!

What you're talking about, the question of how much you should "divvy up" your money into different accounts for different purposes, is something researchers call mental accounting. Richard Thaler is the dude who pioneered research into this phenomenon, and he won a Nobel Prize for it (and his insights into behavioural economics more generally), which just gives you an indication of HOW DEEP THIS RABBIT HOLE TRULY GOES, my friend.

Mental accounting is the technical term for how we think of different pots of money differently. Three common ways we do this:

- You treat money differently based on its source. Money you got as a bonus or a gift or tax rebate is money you're more likely to spend on something fun, and less likely to save.

- You treat money differently based on its "type". It's harder to cash in savings than it is to spend money on a credit card, even though buying something on a credit card makes it more expensive (if you can't pay it back before it starts accruing interest).

- You treat money differently if you've earmarked it for a purpose. We do this when we mentally (or physically) earmark money for saving, bills, retirement, holidays etc.

The thing about dividing money up like this is it isn't true. Money is fungible - which means that a pound is a pound is a pound. In reality, you could always change your mind and decide to spend that earmarked money for something different. But we often don't: once we've mentally allocated money in this way, it's really hard for us to un-allocate it.

Now, mental accounting is neither good nor bad, it's just a thing that humans do. Sometimes, it can lead people to make really bad decisions, like when they should be using savings to pay off high-interest debt but don't, or when we spend tax rebates on nonsense because it feels like "free" money.

But mental accounting can also be a tool that you use to help you reach your goals, like when you give yourself pocket money in a Fuckaround Fund so that you don't accidentally spend all of your savings on Lego sets and box wine (it's been a long lockdown, okay).

So, back to the specifics of your question. Really, there are three different approaches to saving up for all these lovely things that you want:

- Actually open up different savings accounts for each goal. In South Africa, this gets expensive and becomes a hassle as soon as you go beyond 4 accounts. In the UK, the new banks like Monzo/Starling let you open up little savings pockets in the app (SA friends, UK banking is A DREAM, I can't even explain).

- Just lump everything into one big savings account that you call POSSIBILITY MONEY or POTENTIAL PILE OF FUN SHIT or whatever, and just spend out of it whenever you feel like it.

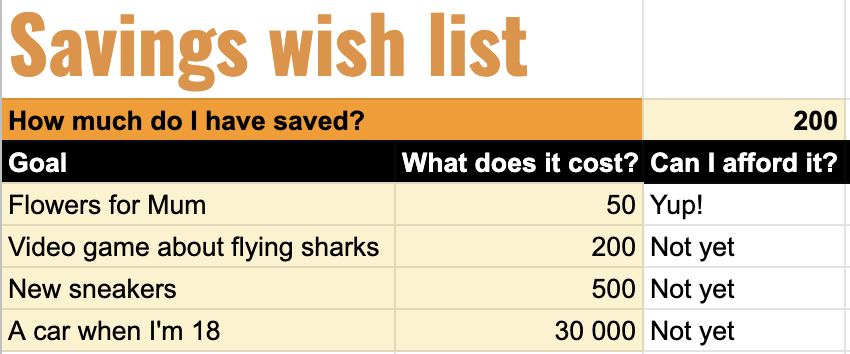

- Some mix of 1 and 2 where you keep the actual cash in a big pile, but also keep a wishlist where you track what money is virtually spoken for. Here, you can copy the one I made for the Teens' Money Mission Control Google Sheet, which tells you when you can afford the next priority on your wish list.

Now, some types of people are extremely motivated by route 1 (saving towards very specific goals). This is a way that mental accounting can be used as a tool: it might be much easier to convince yourself to stash money away by feeling like you're actually pre-purchasing a little chunk of something you really really want, than by just saving for the sake of it. If saving like this helps you to save more overall, go for it. Having a shared family saving goal that you track on the fridge can be a great way to engage kids about money, for example.

Personally, I dislike mental accounting and generally try to resist it. Here's why: I don't like being held hostage by my past self. You've got to understand, Past Sam is an IDIOT. She made a number of extremely questionable life choices and ate way too many greasy chip rolls and did NOT apply enough sunscreen in her 20s, and basically left me to clean up her entire mess... what an asshole. Past Sam wanted a lot of things from her life that I do NOT want. Past Sam once nearly bought tickets to a boat rave in Ibiza. Present Sam likes to be in bed by 10pm on a Saturday.

Here's the balance you must hold onto, though: it turns out that Present You is also kind of an idiot. Yes, don't get too cocky there, Present You! Because most of us are actually pretty rubbish at guessing what spending decisions will make us happy. We forget all the time what actually matters to us, and it's helpful to have a way to remind yourself.

Present Me? Here's a confession: she is absolutely convinced that the one item that will COMPLETE HER and solve every sartorial problem for the rest of her life is a black velvet tuxedo jacket. She's been drooling over photos of them for, like, all of the past two days. Except, last week she was drooling over these cat shorts from Disturbia. And the week before that she was fully committed to buy some chunky 80s jewellery from eBay.

And that's why I think option 3 is the way. It's a balance between not being held hostage by Past You (an idiot), while also not being a slave to the every immediate impulse of Present You (also, it turns out, an idiot). It's a way to help that magical being - the Best Version of You - take the wheel, more of the time.

Here's what that looks like for me: I keep a tab on my Money Dashboard that is the Things Sam Wants list. Every time I'm browsing Instagram and see a new thing that lights up the covetous bits of my lizard brain, I add it to that list. It's how I interrupt my impulse shopping: instead of "Add to Cart", "I Add to List".

My Things Sam Wants list is sorted by category: experiences, adventures, learning opportunities and holidays are at the top, hobby-type things and books come next, and clothes and house stuff is at the bottom. This is a helpful reminder to myself that the things at the top of the list usually make me much happier than the things near the bottom of the list. Because, believe it or not, Present Sam forgets this all the damn time. This list is the way that the Best Version of Me reminds her of what actually matters.

This list is the reason I'm unlikely to ever get around to buying that velvet tuxedo jacket. And good thing too, because I'll no doubt be onto some new obsession by Friday.

Then, instead of keeping a R I G I D S Y S T E M with a bunch of different savings accounts open with specific savings targets, I just have one single pile of cash. This is my Emergency Fund and also my Splurge Fund, in one - a Slush Fund, if you will. Instead of a clear budget of pre-allocated money, I make sure that fund's value always fluctuates within a range (let's say the rule is, "my slush fund can never be less than R60k or more than R120k" for example). The floor of that range is my true "Oh Shit" budget, and I never spend out of it unless it's a true emergency. But your Slush Fund also needs a lid, because at some point you should rather be investing money than keeping it in cash. When my Slush Fund gets too big, that's a reminder to me that I need to go back to the Things Sam Wants list and actually spend some of that cash, probably on something near the TOP of that list (like a holiday). Because NOT spending your savings ever is just another way that mental accounting is defeating you.

And of course, the real beauty of this system is that we're talking here about how to optimise your spending on fun shit like Nike shoes and holidays. You've told me that you've already taken care of the actually important stuff, like making sure you've hidden your retirement savings from yourself, which is one way that using mental accounting as a tool is extremely helpful. If you knew you needed to send your kid to university in 2 years, for example, a separate savings fund for this would probably be a good idea, too.

Really, once you're at the point where you're maximising how you save for fun stuff, you're okay. Stop worrying.

Wishing you velvet tuxedo jackets, kiff Nikes and flying sharks,

Your friend Sam

Updates from Sam-Land

Speaking of actual holidays, this week's post was sneakily pre-scheduled because I'm currently in Cornwall, sans-laptop. Google Images says that Cornwall looks like this:

I am stoked. This has been a long, long, long, loooooooong year, chaps, and I'm excited to switch off for a bit. I'm planning to read books, eat food, go for walks, and do a lot of puzzles (and attend exactly zero boat raves).

I hope you're enjoying the start of spring or autumn, wherever you are :)

Member discussion