Is it safe to invest in a new ETF?

Hello, grownups!

This is a beautiful world, filled with puppies and mountains and salt & vinegar Pringles, but sadly, it's ALSO full of dodgy bastards who are plotting to steal your money. We all have to be on our toes, and make sure we're keeping our hard-earned savings safe from fraudsters.

A couple of weeks ago, I mentioned that Satrix just launched two new low-cost global ETFs specifically for sustainable investing - the MSCI World ESG Enhanced & the MSCI Emerging Markets ESG Enhanced funds ("ESG" stands for "Environmental, Social and Governance"). This is wonderful news for South African investors who want a simple, low-fee global investment that also doesn't feel icky.

But one of you wrote back with some concerns:

I have a question: Does ETF fund size matter?

I’m very keen on the Satrix MSCI World ESG enhanced ETF but because it’s new, the fund size is zero.

My sense is that Satrix itself is solid and looking at the index performance of the World ESG ETF over the past 5 years, I like what I see, but is there a risk in investing in a new fund like this? It looks like the targeted annual TER is only slightly higher than their MSCI World ETF, and I’m willing to take that hit to support and earn from ESG focused businesses, but could the TER end up being much higher? Is it possible that the targeted low fees aren’t achieved?

I love skepticism around financial recommendations. So, I thought this could be a good opportunity to talk about recognising whether an ETF is "safe" to invest in, in general.

Hang on, what's an ETF again?

Picture walking into a supermarket, and seeing a bunch of products lined up on the shelves that you can buy.

Now imagine that instead of buying the products, you could buy tiny pieces of the businesses that MADE those products.

Right, so that's all the stock market is: a place where people buy and sell tiny pieces of businesses. When those businesses make a profit, you get a cut of it.

You get a layer of protection from buying businesses through a real stock market like the Johannesburg Stock Exchange, or the London Stock Exchange, or the New York Stock Exchange. Businesses pay a lot of money to be listed on these exchanges, and there are rules listed companies have to follow. These rules make it harder for companies to be run badly or fraudulently. But it's still not impossible: sometimes, you get a Steinhoff or an Enron.

It's the difference between buying tomatoes from an established grocery chain versus buying tomatoes from a dude in a dark alley who has them stuffed under a trench coat. You MIGHT still get food poisoning from the grocery store tomatoes, but it's less likely.

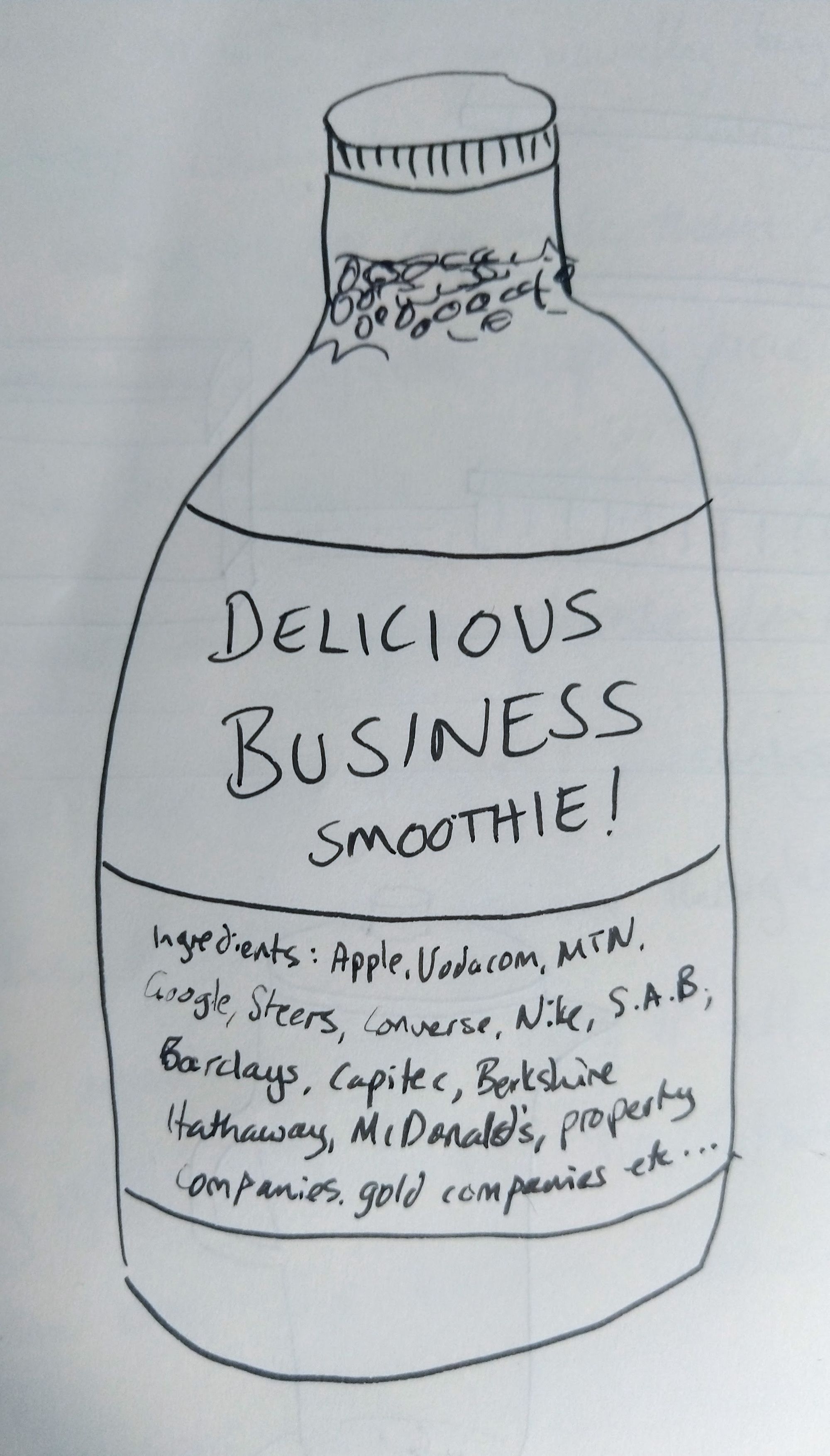

Now, you're a busy and important person, and far too busy and important to spend your life reading the business news (BORRRRING) and figuring out what companies you should be buying. So instead, you buy an ETF (an exchange-traded fund). An ETF is like if somebody took all the companies in the supermarket and put them in a blender, and then sold you pre-mixed smoothie.

The great thing about buying a smoothie, is that one rotten ingredient doesn't matter that much. The more things you've managed to mix in, the less any one company makes up the overall product. So, you get an extra layer of safety by buying ETFs rather than by buying individual shares.

There's always a chance that any one company you buy might end up being the next Steinhoff, or the next Blockbuster Videos. But ALL companies becoming worthless would only likely happen in a true apocalypse situation, where money won't have meaning any more anyway. ETFs let you very easily invest money into businesses all around the world, in a lot of different sectors. They're the shizniz.

Historically, there's no single asset class that's done better over the long term than the stock market (and we have over 100 years of history on this), returning around 7% above inflation. Which means that any time you see a financial product promising returns higher than that, your scam senses should start tingling. There's a new super dodgy probable pyramid scheme going around at the moment called Mirror Trading International that promises 10% a month (which is 214% growth a year). Ha fucking ha.

(TL;DR: a low-fee globally-diversified ETF is the starting investment I recommend to most beginners, and there's a list of them here).

Is it a problem if an ETF is brand-new?

Let's go back to our reader's question.

My sense is that Satrix itself is solid and looking at the index performance of the World ESG ETF over the past 5 years, I like what I see, but is there a risk in investing in a new fund like this?

Satrix, in this case, is the South African company making and selling the smoothie. The recipe for the smoothie is actually from an American company called MSCI. They came up with the "index", which means, the list of which companies should be included in the product. You can buy an identical smoothie from a lot of other companies around the world, like iShares or Blackrock, but right now, Satrix is the only company selling this flavour of smoothie in South Africa.

All ETFs made from the same recipe should perform allllmost identically. So, even though this particular Satrix ETF didn't exist until recently, you can see how it would have performed by looking at the performance of other ETFs made from the same index.

(Here's another example. A different index you might have heard of is the S&P 500, which is a recipe created by a company called Standard & Poor, which is made up of the 500 biggest companies in America - you can buy S&P 500 flavoured ETFs from LOADS of different companies, and the recipe is the same every time, although the COST might differ, which is why you'd want to shop around.)

Satrix is registered with the Financial Authority (FSCA), who are like the food inspectors of the financial sector. And you definitely should make sure that you only invest through registered companies. This is another layer of protection.

But the nifty thing about ETFs is that each one actually exists as its own entity, outside of Satrix. Satrix doesn't technically OWN the smoothies it sells, or the shares that make it up, it just manages and markets them. That means that even if Satrix went bankrupt, or their CEO personally absconded with all their money and fled to the Caymen Islands on a yacht with Ryan Gosling, your ETF is still fine.

I reached out to Kingsley Williams, the Chief Investment Officer of Satrix, who confirmed this for me. "As attractive a proposition as fleeing to the Cayman Islands, on a yacht, with Ryan Gosling may be, our financial services sector is extremely well regulated and would prevent this from happening," he said. "Since the assets of the fund are not in the Manager’s (Satrix) name they are protected from the insolvency of Satrix. Also each collective investment scheme [like this ETF] is governed by a trust deed which falls under the authority of the FSCA [the food inspectors]. The FSCA has the authority to inspect the work of the trustee and the manager of the fund which makes things like absconding with the assets of the fund very difficult."

Ironically, this means that in South Africa, your money is actually safer in an ETF than in a bank, because bank deposits aren't actually insured in SA (although there are new laws being passed right now to try to fix this; and bank deposits are insured in many other countries).

What if the ETF is shut down?

Very rarely, ETFs do close, but this doesn't just happen willy-nilly.

For an ETF to close, there has to be a ballot where a percentage of investors have to agree to this, and the whole process is audited closely by the FSCA. If the investors agree to close the fund, then usually they're offered the option of either swopping their holdings in that ETF with an alternative one, or they're paid out the current value of the ETF, which they can then invest in something different. This is a schlep if it happens, but it happens rarely (Satrix, for instance, has never closed any of its ETFs to date), and it's a hassle rather than a financial disaster.

You can watch an ETF closure play out right now in China, where Vanguard (another smoothie-selling company) is moving their Hong Kong office to Shanghai and shutting their Hong Kong-based ETFs. Their investors are grumpy about it but aren't losing money: their ETFs are being transferred to new investment managers or liquidated, in which case they get their ETF's value in cash, and can go invest it somewhere else.

What if the fees end up being higher than advertised?

Our reader was worried that the TER (total expense ratio; i.e. how much Satrix charges you for making/managing your smoothie) would end up being higher than advertised:

It looks like the targeted annual TER is only slightly higher than their MSCI World ETF, and I’m willing to take that hit to support and earn from ESG focused businesses, but could the TER end up being much higher? Is it possible that the targeted low fees aren’t achieved?

Kingsley responded to this: "Regulations prevent management fees being increased without giving 3 months’ notice to investors prior to increase. The TER can increase without prior notice if other allowable costs such as bank charges, audit or trustee fees increase or are included in the fund. Issuers generally stick to targeted TERs and will waive their management fee if other costs in the TER increase. However, this is up to the issuer."

In other words, it IS possible that the TER could end up being slightly higher. But because it's a brand new fund, and Satrix wants it to do well, they're likely to "swallow" additional fees at first rather than passing them on to the investor (but they're not required to). In fact, since announcing this product, Satrix has already lowered the TER on their ESG funds to match their non-ESG funds, so that investors aren't penalised for preferring an ethical fund. Good on them!

And if they did raise their TERs in future, you would get 3 months' notice on this, which would be plenty of time to switch to a different ETF if you wanted to.

(Sidebar for the finance nerds: a small fund size really can be a problem for unit trusts, in a way that they aren't for ETFs. A unit trust typically receives/pays for flows in cash, which cause transaction costs and fee drag which might be quite big relative to the fund size; but ETFs usually receive/pay for flows via a basket of underlying shares, thereby avoiding transaction costs.)

So, is investing in a brand-new ETF safe?

Ja, it's fine. As long as you're sure you're buying it from a trustworthy company that's regulated by the financial authorities.

The big risk with an ETF is underperformance: it's definitely possible that there will be (cough cough) a global pandemic or something and the whole world's economy will get pummelled, so you should make sure that you only put money into an ETF if it's money you're saving for the long term, so that you can withstand the temporary ups and downs of the stock market. But that's not the same thing as a fraudster running off with your life savings.

Sure, there's always some risk in doing anything, and there are some wild, highly unlikely scenarios one could imagine where you'd lose all your money investing in an ETF. But just remember that one of the riskiest things you can do with your money is not invest it at all, because inflation will just nibble its value away year by year.

Wishing you delicious business smoothies,

Your friend Sam

Updates from Sam-Land

Whatcha doing tomorrow morning, lovelies? I'm hosting a webinar especially for teens. We'll be talking about the basics of earning, spending and saving, and how not to turn into an extremely boring adult. Bring your favourite young person! Register here.

Member discussion