What buying a new car in my 20s did to my net worth

Hello, grownups!

Today I want to tell you a quick story about the stupidest purchase of my 20s: a brand new car (AKA the She-Hulk).

In my mid-20s, I had a job working for an ad agency (because what else do you do with a degree in literature and religious studies?). I got promoted to a role that I was dramatically under-qualified for, that required me to be in front of clients occasionally. It was all very thrilling! And also nerve-racking, since it was surely just a matter of time before everyone else realised I was an imposter who had nooooo damn idea what I was doing.

In a misguided attempt to get other people to take me more seriously, I decided to use most of my new promotion money to buy a new car. Now, I had a perfectly good car already: an ancient Corsa Lite named Tony Moneo. It didn't have aircon, power steering, or even a reliable handbrake, but it DID have a rocking sound system and dozens of bumper stickers. Most importantly, it did the job of taking me places perfectly well.

I decided to buy a new car pretty much on a whim driving home from work one day. There happened to be a Hyundai dealership on my route home, so that's where I went. It took me about ten minutes after arriving at the dealership to decide on a make and model. Yes, friends, I put less thought into buying a car than I usually put into buying a pair of jeans. Young Sam was not very smart about money.

I chose a cute blue little i20. I couldn't actually afford it, but the very "helpful" salesman moved some numbers around, added a giant balloon payment, and then POOF! Suddenly I could. (Friends, never never take a balloon payment in a car loan; trust me).

I really loved driving that Hyundai... for about two weeks. Then, to be honest, I seldom thought about it. But for the next few years, that Hyundai continued to steadily drain money out of my bank account anyway. Those were the years when I was spiralling deeper and deeper into debt, but selling the She-Hulk seemed impossible. It felt like it would be too embarrassing, after having posted photos of my shmancy new car all over Instagram and shown it to my parents in an attempt to reassure them that see, it WASN'T so silly to spend four years getting an Arts degree.

It really was the dumbest thing I've ever bought. Usually, our biggest financial mistakes happen when we spend money to try to fix our emotional problems. It seldom works.

A lot of people who don't know me assume I'm a miser. I'm really not: I love spending money. I just hate wasting money. To me, money is wasted if the amount of joy or meaning you trade it for isn't worth the cost.

Wasting money makes me mad, because there is a finite amount of money you'll have in your life. And, more importantly, a finite amount of time.

When salesmen sell you debt-based products, they try to keep you focussed on the monthly repayment amount. They want you to think that asking "can I afford this" means "could I pay this repayment amount every month?" But there's a totally different way to evaluate big financial decisions like this: "what will this decision cost me overall, and what could I do with that money instead?"

So let's compare two different approaches to buying a car: buying a new car with a car loan, versus buying a second-hand car with cash.

For this example, let's imagine that I want to buy a Hyundai i20 like the She-Hulk (it was, after all, a perfectly fine car).

Scenario 1: brand spanking new car

You can buy a brand new Hyundai i20 1.2l Motion for R278,500, for the cheapest model. I plugged this into the Wesbank vehicle finance calculator on the presets, and it spits out these figures:

- Cost of car: R278,500

- Payment term: 72 months (6 years)

- Interest rate: 13%

Let's also assume that you have to service the car occasionally (this specific deal comes with a warranty but not a service plan). Because it's a brand new car, let's say that you only have to keep R2,000 a year aside for this.

Overall, this deal will cost you R5,598 a month. Over the 6 years of your car loan, it will cost you you R403,028 in total.

Sidenote: I'm ignoring petrol and insurance, just for simplicity.

At the end of the 6 years, your Hyundai will be worth about R90,000 if you sell it.

Upsides: you get a spanking new Hyundai, and you can get it immediately. You're also less likely to deal with breakdowns and mechanical issues. These are all very nice things!

Scenario 2: buy a second-hand car in cash

You can buy a second-hand Hyundai i20 1.6l GLS for R70,000. That's a 2010 model, so it's pretty old. Let's also budget a full R10,000 a year for repairs and maintenance.

You'd already budgeted R5,598 a month to buy the new car. Let's imagine that, instead, you save that amount of money every month until you can afford to buy the car cash. That's going to take a year, during which time you'll be bumming lifts, riding a bike or dealing with public transport.

Now, here's the fun part. After you've bought your car cash, let's say that you keep saving that same amount every month. Because you're saving for 5+ years, it's smart to put that money into the stock market through a diversified ETF. Let's assume you get an average of 7% a year growth, after inflation (that's the long-term average for equities).

Using the "investing monthly" calculator in the Money Dashboard, you'll see that those savings would be worth about R400,000 after 5 years. That's enough money to, for instance, buy a plot of land in Hermanus, also in cash. It's probably also enough money for you to take a year-long sabbatical, or pay for full undergraduate degrees at Wits University for two children.

Who's the winner?

At the end of 6 years, here's where you stand:

| New car | Used car | |

|---|---|---|

| Total spent | R403,028 | R403,028 |

| End value of car | R90,000 | 0 |

| End value of savings | 0 | R400,000 |

| Upsides | New car, no bumming lifts for the first year, fewer mechanical issues | Everything else you can do with R400k |

So, what's the better decision? The answer is: it depends what you value. For me, a new car is pretty much never going to be worth it, because I don't actually give a shit about cars, and there are many things I'd much rather do with all that money.

But there are other people who sincerely love cars, and heck, those people really should spend as much money on cars as they can.

The point is: make a thoughtful decision about big purchases like this. Think through the lifetime cost of the purchase, and not just the amount you pay every month. Consider the opportunity cost: what is everything else you could do with the money instead.

I'm talking about cars here, because it was a choice that affected my own 20s significantly, but we waste money on a bunch of things that don't bring us much value: energy bills, insurance, fancy cellphone contracts...

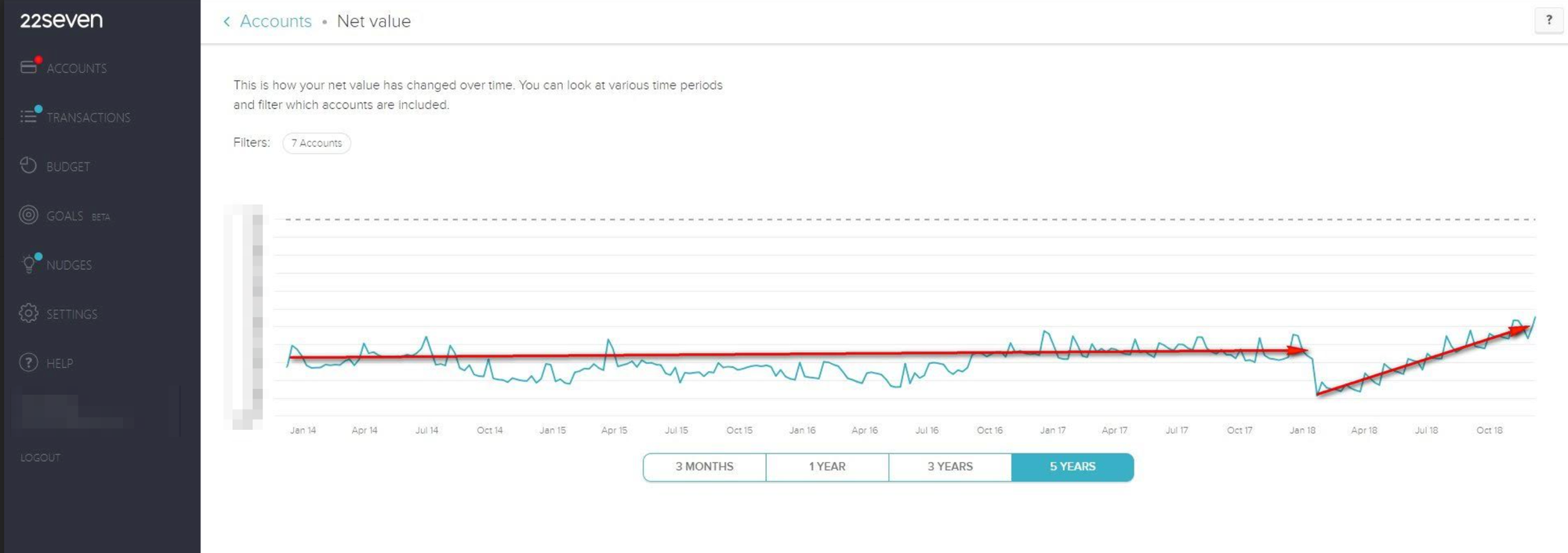

If you've already made big financial decisions, it's important to re-evaluate them from time to time, too, based on your financial situation today. A couple of years ago, a reader sent me this graph. It's a screenshot of his 22seven account, showing his net worth over time. After reading my money book, he decided to take cash out of one of his savings accounts and use it to settle his car loan. You can see what happens to the graph when he did.

You always have choices. Use them, because your money and your life are both limited.

Spend money! But don't waste money.

Wishing you bumper stickers and thoughtful financial decisions,

Sam

How to start a side-hustle

My buddy Nic Haralambous just released the ultimate guidebook to starting a side-hustle. I've read it and it's great: practical, inspiring and full of truth-bombs (I particularly loved the section about how new entrepreneurs often get caught up in all the "formal" stuff you think you need to start a business, like business registration or business cards, before they've actually tested that people want to buy what they're selling). It's out now, and it's the playbook you were looking for if you were thinking about starting a side-hustle but didn't know how to start.

Updates from Sam-Land

Somehow, despite having followed our lockdown rules rigorously, I've managed to pick up a flu virus (HOW??? Did it climb into my window while I was asleep???). It's not Covid (we tested), but I've been quite ill this week. Please appreciate how much I love you that I wrote you a newsletter this week anyway! I've otherwise spent the week lying on the couch reading Mark Gevisser's The Pink Line (which is wonderful) and binging Ted Lasso (also wonderful). Please beam me healing vibes!

Member discussion