The market crashed. Should I buy the dip?

Hey buddies. How are you holding up over there? Things are so weird. I know that all of you are dealing with your own unique gumbo of unemployment, sickness, worry, cabin-fever, hunger, sadness, grief, exhaustion. I'm so sorry. I'm beaming love at each and every single one of you.

I've been getting quite a few emails recently from readers who have watched their stock market investments get pummeled, and are asking if they should respond to this by buying more shares, or if they should wait it out, or if the stock market is just broken forever now and we should just start investing in potable water and toilet paper futures.

My tl;dr answers to these questions are:

- It depends.

- It depends.

- Probably not.

Here's one of those questions, from a UK reader:

I just wanted to get your opinion on something, I have bond with [a bank] which is about to expire, I'm going to withdraw £5k from that bond and want to invest it into funds with Hargreaves Lansdown across multiple industries and countries but concerned that right now is not the best time to get involved.

The plan is to put £1k into 5 different funds for the next 10 years and add £50 a month into each fund, should I wait a couple of months of this whole corona stuff to blow over or is the market in a good place for people like me to buy?

On the surface, a market-dip is a great time to buy investments. Underneath all the finance-speak waffle, the stock market is a collection of businesses that you can buy tiny pieces of. When the stock market is down, that means you're buying pieces of businesses at a huge discount. The market's on sale! Theoretically, if you buy the shares at their cheapest, and hold onto them until the market bounces back, then you can make a bigger profit. This idea is called "buying the dip". And while I'm normally against any type of market-timing for regular people, I do believe that continuing to buy shares through a crash is an important part of a long-term investing strategy.

But it's a little more complicated than this, because it really does depend on your individual circumstances. When people ask me if they should be trying to "buy the dip", I usually ask them three questions:

- Have you got any high-interest debt?

- Can you wait 5+ years to get this money back?

- Are you speculating or investing?

Consideration 1: have you got any high-interest debt?

If you have high-interest debt (credit cards, personal loans, store cards etc.) you should pay that off before you start investing. Almost always. Say it with me: Klap the debt before you invest.

The exception to this rule is tax-protected retirement savings, especially when they come with some kind of employer savings match.

Consideration 2: can you wait 5+ years to get this money back?

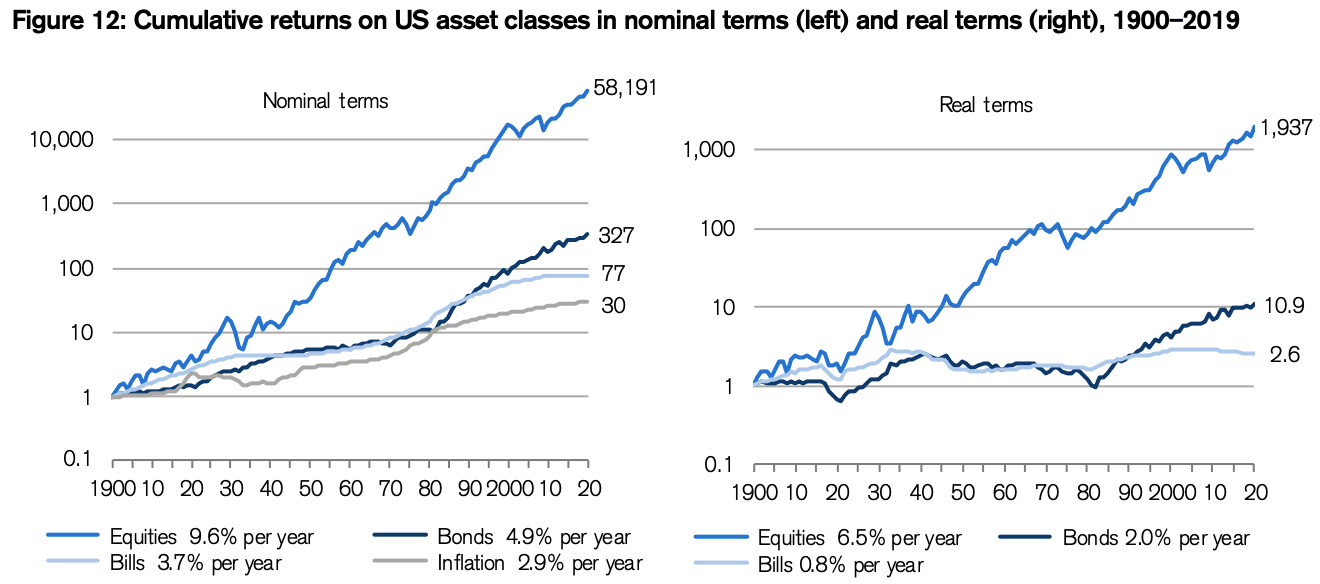

Here's the thing about the stock market: over its 120-year+ history, it's crashed many times. Every time, it's recovered... eventually. It's pretty dang likely that it will recover this time, too... eventually. The trick is in that "eventually". No-one knows if that "eventually" is going to be in 5 months or 5 years or 15.

See this blue line? That's the U.S. stock market over the past 120 years. Lots of wobbles, but it ultimately wobbles up.

If we continue to have an economic system that looks remotely like the one we currently have now, the stock market will recover (and if the whole economic system changes fundamentally, then nothing you do with your money now matters anyway).

Here are the best and worst rolling periods in the history of the U.S. stock market:

Annualised returns of the S&P 500

| Market high | Market low | |

|---|---|---|

| 1 year | + 53.99% (1933) | - 43.34% (1931) |

| 5 year | + 28.56% (1999) | - 12.47% (1932) |

| 10 year | + 20.06% (1958) | - 1.39% (2008) |

| 15 year | + 18.92% (1999) | - 0.64% (1943) |

| 20 year | + 17.88% (1999) | + 3.11% (1948) |

So, the worst 5 year period were the years 1927-1932, when the stock market lost 12.47% of its value. There have been 15 year periods when the stock market lost money, but there has never been a 20 year period when this is true, so far. The stock market might not bounce back quickly. So, you need to be sure that you can live without this money for as long as the stock market's gonna take to recover.

That's why you shouldn't be touching the stock market unless you have a healthy emergency fund. I'll level with you, friends: a lot more of us are going to lose our jobs before this is over. Do you have enough cash savings to cover 6 months' worth of expenses, if you need to? If you don't, that's your priority right now.

This also means that you should be careful buying shares right now if you're close to retirement, or if you're already retired. If that's you, do buy some shares, but also balance your portfolio with lower-risk asset classes like bonds.

There's a cost to not investing your money in the stock market: it's the best performing asset class over the long run, so the extra risk is worth it if you have time on your side.

Consideration 3: are you speculating or investing?

Speculating means taking advantage of the wobbliness of the market to buy and sell assets quickly for a profit. It's a lot like gambling, because you're essentially betting money on the movement of an asset in the short-term. It's also a lot like gambling in that most people lose money doing this.

Why? Because it's a zero-sum game (your profit is someone else's loss) and the average person is much worse at this than they think they are.

Investing means buying assets that will make a profit and increase in value over the long-run, regardless of the short-term price movements. It's less like gambling and more like planting seeds.

Trying to find exactly the bottom of the market and buy assets at that moment is speculating. The odds are overwhelmingly against you being able to guess where the bottom of the market is, and I beseech you in the magnificent name of David Attenborough that you don't try.

I also implore you not to try to pick individual shares right now, unless you have built up a lot of expertise in doing this. The stock market will recover, yes, but many individual businesses will not. The world will recover but some individual countries are going to have a very difficult decade.

How do you get around this risk? Diversification, my buddies. Instead of making bets on individual business, buy index ETFs. Instead of pinning your hopes on your own country's economy (or the U.S. economy, or any other economy), buy global funds. Instead of trying to time the bottom of the market, just keep putting the same amount of money in, every month. It will average out over time.

That's not to say that I'm cavalier about the fact that people are losing frightening amounts of money right now, friends. Shit's bad. Pensioners' retirement savings have dried up. The cold mathematics of the drawdown recovery rule means that stock market crashes are even more devastating to your portfolio than they look on paper. But the only way to get through them is to capture the upside as well as the downside, which means buying the shares when they're cheap, i.e. now.

What should our reader do?

So, after all that pre-ramble, let's get back to our reader's specific situation:

I have bond with [a bank] which is about to expire, I'm going to withdraw £5k from that bond and want to invest it into funds with Hargreaves Lansdown across multiple industries and countries but concerned that right now is not the best time to get involved.

The plan is to put £1k into 5 different funds for the next 10 years and add £50 a month into each fund, should I wait a couple of months of this whole corona stuff to blow over or is the market in a good place for people like me to buy?

Reader, if you don't have high-interest debt, and if you do have a healthy emergency fund, and if you're happy to not touch this money for 5 years, then yes, you're exactly the kind of person who should be investing right now. You're doing the smart thing, splitting your money across multiple countries and industries, and it sounds this is all part of a well-thought-through long-term financial plan.

As weird as it seems, as the world slides into what often feels like a fever-dream nightmare, your investment strategy now should probably be pretty much the same as it was before this all happened. Trust past-you. They put together a good plan.

The only thing I'd suggest is not "seeding" the funds with that £5k all in one go. Rather drip it in over a couple of weeks, and do keep investing consistently over the next few months, regardless of what the market does.

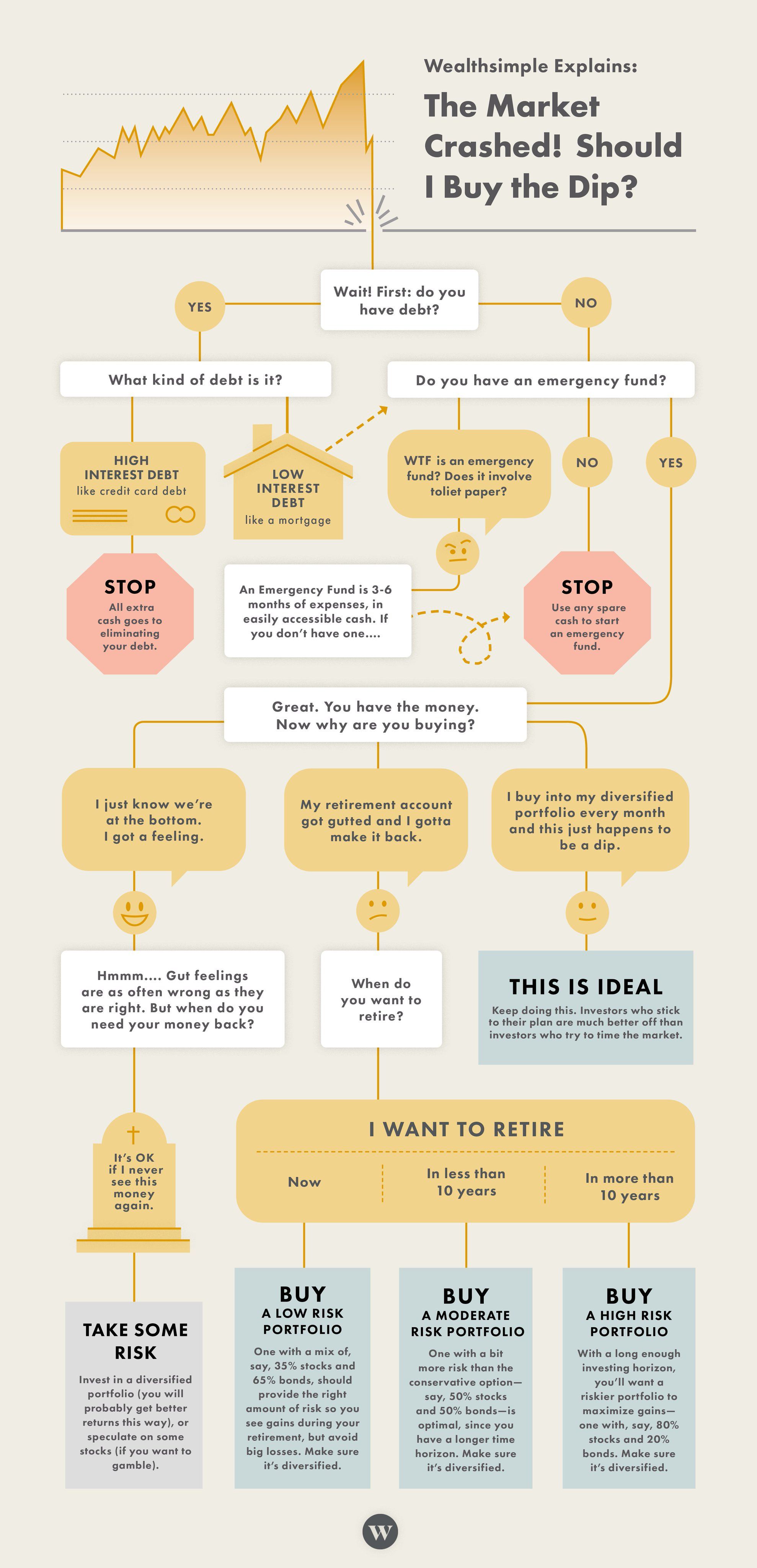

I'll leave you all with a nice little summary chart from Wealthsimple.

Member discussion