How does compound interest apply to ETFs, and where would you invest for a teen?

Hello, grownups :)

Today I'm tackling two reader questions. Let's hop right in, shall we?

I read and took in all that you said about the magical properties of compound interest. I have got it, I am sold. But even after having read your book and browsed yours and other financial websites, I still don’t understand how to get compound interest anywhere other than a bank account, where I can understand the simple notion that any interest gets re-invested. But how would I get compound interest with an ETF ? Sorry, this feels like a very, very dim question. But if I want to follow all your advice about getting a low-fee, very diversified ETF, then can I still take advantage of the compound interest effect? HOW?

This is an EXCELLENT question, actually. You're quite right that it's not technically interest doing the work on ETFs. You're still getting compounding returns, but in an ETF, these returns are a combination of the value of the underlying shares increasing (what we'd call "capital gain") plus dividends. Some ETFs automatically reinvest dividends for you, and other don't.

--

It's worth taking a step back to talk about why your money actually grows when you invest in it ETFs (the answer is not "Leprechauns").

An ETF is a clever way to let you buy a tiny slice of a basket of underlying shares (amongst other things, but I'm going to talk here about share-based ETFs). It's a lot like a mutual fund, except the ETF itself is traded on a stock exchange like any other stock, which makes it a bit more flexible and transparent.

But don't worry about the ETF layer. The important bit is the businesses that underlie it. When you invest in an ETF, you're indirectly buying tiny pieces of those businesses. Your money grows because those businesses are making a profit (hopefully), which they're either paying out to their shareholders or re-investing to grow themselves.

Imagine one of the businesses you own a tiny piece of, through your ETF, is Apple. This year, Apple makes a profit. What are some things they can do with that profit?

- They could develop new products.

- They could buy up another business.

- They could build new manufacturing facilities or Apple Store branches.

- They could expand into new markets.

- They could just pay it out to their shareholders.

If they do #1-4, they're doing those things because they believe that they will grow the value of Apple as a business. They've re-invested their profit. You, as a shareholder, benefit from them doing this, because your shares in their business are now worth more (capital growth).

If they do #5, then you just get the cash. With some ETFs, you literally get a cash payout four times a year (these are called "distributing" ETFs). You will have to re-invest this profit yourself to get the compounding effect. With other ETFs, your dividends are automatically used to buy up more units of the ETF, so you get the compounding effect automatically (these are called "accumulating" ETFs).

Some people buy accumulating ETFs when they're young, and move to distributing ETFs when they're older, and need to start living off their investments.

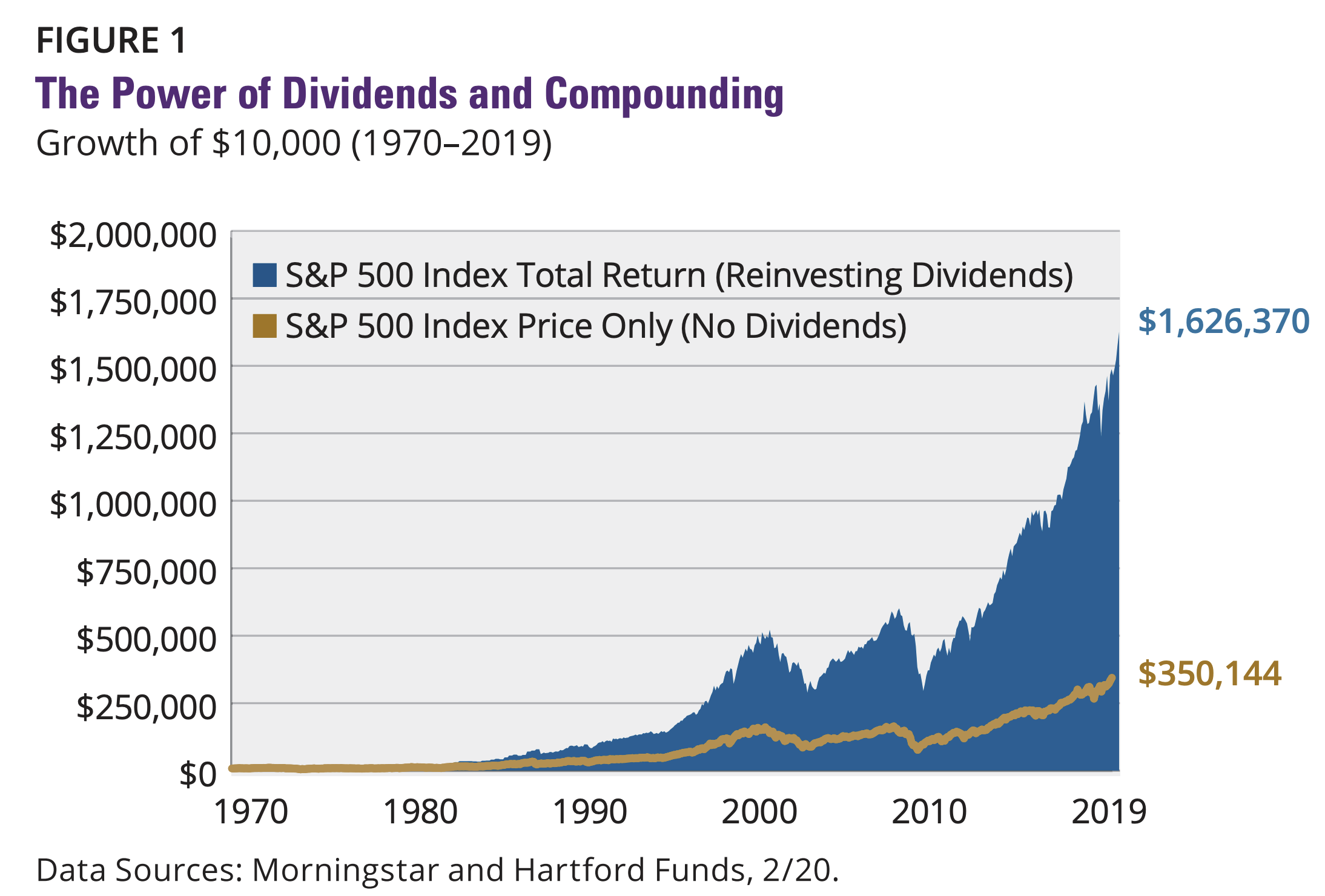

Fun fact (fun for finance nerds, anyway): over the past 50 years, the compounding effect of reinvested dividends have been responsible for 78% of the total return of the S&P 500 index (i.e. capital gain was only responsible for 22% of the return).

--

So, absolutely: when you're investing in ETFs, you should be hoping for compounding returns, not specifically compound interest, but the effect will be exactly the same. The beautiful math of compounding, that was described in the book through an elaborate rats metaphor, will still apply to ETFs just like it does to savings accounts.

Of course, the one big difference between ETFs (or stocks in general) and savings accounts is that the returns on ETFs can compound down as well as up. Sometimes the businesses in your ETF will make a loss, not a profit. That's why it's so important to reduce your risk through diversification.

I still like to refer to all of this informally as compound interest, mostly because it's a familiar term to people. Generally, in the world of money, I think of ‘interest’ as being the money that you earn for investing your money or putting it to work in the world (good interest), or the cost of using someone else’s money (bad interest).

My teenage son has come into a small lump sum of R25,000 and I want to invest it for him, not to be touched for at least ten years. The one other factor is that of course he might want to leave South Africa ☹. So where would I stick this lump sum to grow quietly, preferably in dollars or similar? I’ve read all you’ve said about EasyEquitites and global tracker funds … do I head there?

Lucky teen! I hope he got the money from doing something extremely cool, like monetizing a complex TikTok dance or being Batman's sidekick for the summer. And good on you for wanting to put that money to good work, rather than letting interest degrade its value.

My general rule of thumb for investing is, the longer you can wait for the money, the more of it should be in equities (i.e. shares). Equities have historically been the best performing asset class, but can be very "wobbly" in the short-term. At a 10-year time frame, I'd definitely be looking at a low-fee ETF that tracks the whole world. I can't advise you on exactly which one you should pick, but here's a list of ideas to jumpstart your own research.

Your boy is globally-minded, so you're smart to be thinking about investing in something that's not tied to South Africa's economy. There are two ways to do this:

- True offshore funds, where you first convert your rands to a different currency (like US Dollars) and buy the fund directly in another country. You can do this on EasyEquities or global platforms like Interactive Brokers. You can use an app like Shyft to swop your ZAR for USD.

- South-African based offshore funds (rand-denominated), where you buy shares in a locally-registered ETF and that company then buys up the international funds on your behalf. There are a lot of options like this now. EasyEquities offers many, or you could look at Coreshares or go directly to Satrix.

There are pros and cons to either approach: taking money properly offshore adds an extra layer of protection in case things get extremely weird in SA, but moving money into USD is expensive and increases your investing costs (which reduces your return), and it's a hassle. True offshore investments are also taxed differently to SA-based offshore funds, but it's impossible to tell before-hand which will be better (basically, if the rand weakens, then the true offshore fund is the winner; visa-versa if the rand strengthens).

For R25k I would personally just stick to an SA-based global fund and focus on optimising costs & hassle now rather than trying to predict the future, but you should do your own research about this, and consult a fee-based financial planner if you need extra advice.

You can either open the investment in your teen's name, or your own. If you put it in his name, then there's always the risk he'll withdraw it early to spend it on a wild shopping spree when he turns 18, but it's your job as his parent to teach him solid money skills so he doesn't do this. The fact that you're writing to me now with this question makes me confident that you will!

The advantage of it being in his name, not yours, is that he's more likely to be under the capital gains tax threshold in the year when he decides to sell that investment, than you are.

You could also consider using his tax-free allowance for this, which is like an invisibility cloak that hides the investment from the tax-man completely. The downside of doing this is that if he withdraws it in his 20s or 30s, it's using up some of his lifetime TF allowance which he could otherwise be using to fund his own retirement, as brilliant Stealthy Wealthy suggests here.

Let's just do some back-of-the-envelope maths here. Using the lump sum investment calculator on the Money Dashboard with a 13% growth rate (6% inflation + 7% average real growth on equities), that would predict that the 25k could be worth R90k in 10 years. Capital gains tax could take a real bite out of that, so using the TFSA allowance definitely seems worth considering.

I hope that your son enjoys his Batman money!

Wishing you all invisibility cloaks, compound interest and magical Leprechauns,

Your friend Sam

Updates from Sam-Land

The UK's daily Covid death rate is slowly creeping down to the single digits, and the country is starting to open up again. It's simultaneously joyful, terrifying, confusing and wonderful. I can finally start trying to... make friends in my new country, maybe?

Readers who are in places where things are still feeling out of control, I'm so sorry. I'm holding you in my thoughts.

I've been thinking a lot about mental health armour: the small things you can do that give you greater resilience during rough times. One of the bits of mental health armour that's been particularly helpful to me recently is making a weekly goal tracker in my journal, where I keep track of the most important things I have to do every week.

I try to make sure that these goals support a general froo-froo "theme" I give each season (this is an idea I took from CGP Grey). I followed up the Winter of Small Joys with the Spring of Gentleness, and am now in the Summer of Excavation. Having these little rituals and goals is giving my time structure and purpose, and helps me to feel less adrift.

- Can I interest you in 20% off Marvel's Jessica Jones: Playing with Fire? Use the code SOTWJJ at this link. You're welcome!

- Magpies, the novel I'm writing with Dale Halvorsen, has 66,070 words of a first draft! It is our misshapen brain-baby and I love it. We're set to finish this draft by the end of the month, when we'll take a break for a couple of weeks so we can tackle the edits with fresh eyes.

- I've always wished there was an app that would let me automate my financial strategy, like a customisable money autopilot in my pocket. So, Lettuce is thinking about how we might build this. I'd love your thoughts!

- Some random things that have been bringing me joy recently: collaborative story-telling game Storium, the book Girl, Woman, Other by Bernardine Evaristo, the boardgames Mysterium and Codenames Pictures, Rebecca Haysom's Drawing with Mindfulness online art classes, 30 Rock, and the Fate roleplaying system (some friends and I have been playing a Star Wars game where I play a toddler Hutt wannabe crime-lord named Flim-Flam the Formidable).

Member discussion